|

Cybertelecom

Federal Internet Law & Policy An Educational Project |

|

Internet Backbones & Interconnection :: Policy: | |

|

|

Historically, the Federal Communications Commission left the Internet backbone market unregulated, as explained in an excellent paper by Michael Kende.

In summary, telecommunications providers are subject to common carrier regulations that ensure nondiscriminatory access to end users; together with antitrust enforcement, these regulations serve to protect against anti-competitive behavior by telecommunications providers with market power. In markets where competition can act in place of regulation as the means to protect consumers from the exercise of market power, the Commission has long chosen to abstain from imposing regulation. For this reason, providers of services that combine telecommunications with computer services are not regulated as common carriers. [Kende p 12]

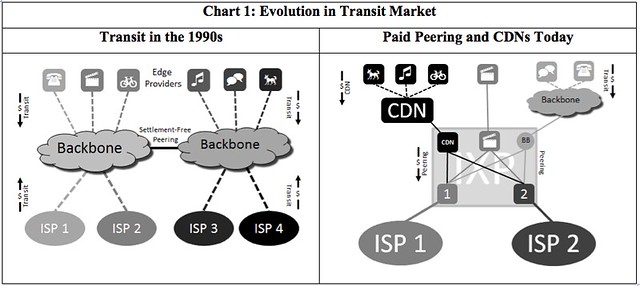

The Internet market had evolved. In the 1990s, Tier 1 backbones were indispensible and were accused of anti-competitive behavior. In the 2000s, service providers works hard to bypass expensive transit through such mechanisms as donut peering or CDNs. By the 2010s, broadband Internet Access Service(BIAS) providers had gained significant market share in terms of eyeballs and gained control of interconnection. BIAS providers went from paying for transit service to exchange traffic with the full Internet - to being paid by edge providers and CDNs in order to access the BIAS' eyeballs. This led the FCC to express concern in the 2015 Open Internet order, placing BIAS Internet interconnection under Title II authority. The FCC also expressed concern in the AT&T/DirecTV Merger Order. During this time, the Comcast / TWC merger was also blocked.

The US Government built the first Internet backbones

- DARPA built the 1st backbone: The ARPANet.

- NSF built the backbone The NSFNet, building a national network dedicated to long distance traffic exchange, which interconnected with regional networks, which interconnected with local networks.

- Other federal networks included CSNET, DISN, DREN, ESNET, and NSI

- NSF gave birth to the commercial backbones when it privitized the NSFNET and built the NAPs (IXPs) (see also CIX)

The USG continues to operate several of its own backbones.

ARPANET 1969 DOD ARPA Operational: Funding CSNET 1981 NSF Operational: Funding FIX 1989 Various Operational: Funding NSFNET 1985 NSF Operational: Funding NAPs 1995 NSF Operational: Funding (model for Internet eXchange Points) Computer Inquiries / Steven's Report 1966 - 1998 FCC Classified as "information service" (Internet backbones were an information service provisioned over common carrier telecommunications); unregulated; Policy objective was to open up telecom platform for benefit of "information services" First Sec. 706 1998 FCC FCC petitioned to intervene in Internet interconnection; concludes market is competitive and intervention is not merited Second Sec. 706 2000 FCC FCC petitioned to intervene in Internet interconnection; concludes market is competitive and intervention is not merited Digital Handshake 2000 FCC Working Paper NRIC 2001 FCC Advisory committee recommends publishing of peering policies GAO 2001 GAO GAO Paper recommends FCC monitor Internet backbone market MCI / Worldcom 1998 FCC / DOJ Merger approved with conditions: must divest of MCI backbone ICAIS 2000 ITU / FCC Resolution D.50 would regulatorily treat backbone interconnection in the same manner as telephone interconnection. US takes a "reservation" from the treaty. WCOM / Sprint 2000 FCC / DOJ Merger blocked Bell Atlantic / Genuity 2000 FCC / DOJ Merger approved with conditions: must divest of GE backbone WCOM / Intermedia 2001 FCC / DOJ Merger approved with conditions: must divest of Intermedia backbone SBC / AT&T 2005 FCC / DOJ Merger approved with conditions: must post peering policies; must maintain peering interconnections Verizon / WCOM 2005 FCC / DOJ Merger approved with conditions: must post peering policies; must maintain peering interconnections AT&T / Bell South 2007 FCC / DOJ Merger approved with conditions: must post peering policies; must maintain peering interconnections TW Petition re VoIP interconnection 2006

2011FCC iVoIP Interconnection required Centurylink / Qwest 2011 FCC / DOJ Merger approved Centurylink / Savvis 2011 FCC / DOJ Merger approved Level 3 / Global Crossing 2011 FCC / DOJ Merger approved Telemedicine Pilot 2007 FCC Universal Service National Broadband Plan 2010 FCC No Action BTOP 2010 NTIA Funding Condition Open Internet 2010 FCC No Action Netflix 2010-14 FCC Interconnection disputes involving Comcast and other broadband Internet Access Service providers Universal Service Inquiry 2011 FCC Inquiry PSTN Transition 2011 FCC Inquiry Inquiry into Congestion 2014 FCC Inquiry Level 3 / TWT 2014 FCC Approved without comment Open Internet 2015 FCC Interconnection between BIAS and upstream providers falls under title II Comcast / TWC 2015 FCC / DOJ Merger blocked AT&T / DirecTV 2015 FCC / DOJ Merger approved with conditions: must submit interconnection agreements to the FCC Charter / TWC 2015 FCC / DOJ Approved with conditions Altice / Cablevision / Suddenlink 2015 FCC / DOJ Approved Centurylink / Level 3 2016 FCC / DOJ Application to be filed Dec. 2016 Verizon / XO 2016 FCC Merger Approved Without Conditions See also

European Interconnection Disputes Computer Inquiries / Steven's Report

The Computer Inquiries created the dichotomy between regulated basic telecommunications service and unregulated enhanced services (aka information services). Basic services were regulated for the benefit of enhanced services. The goal of the Computer Inquiries was to create an open communications network upon which the promise of the computer era could be fulfilled. This begged the question of whether Internet backbones were basic or enhanced services. In the 1998 Steven's Report, the FCC stated:

52 We find, however, little to no discussion of this issue in the record. Accordingly, we do not believe that we have an adequate basis for resolving this matter in this Report. Moreover, we believe that we need not resolve the issue in order to address the important issues raised by the Appropriations Act. The regulatory classification of protocol processing is significant to the provision of universal service only to the extent that it affects the appropriate classification of Internet access service and IP telephony. We find, however, for the reasons explained below, that Internet access services are appropriately classed as information services without regard to our treatment of protocol processing. Similarly, our discussion of the regulatory status of phone-to-phone IP telephony is not affected by our resolution of the protocol processing issue. The protocol processing that takes place incident to phone-to-phone IP telephony does not affect the service's classification, under the Commission's current approach, because it results in no net protocol conversion to the end user. Finally, when a facilities owner provides leased lines to an Internet access or backbone provider, it does not provide protocol processing.

55. "We conclude that entities providing pure transmission capacity to Internet access or backbone providers provide interstate "telecommunications." Internet service providers themselves generally do not provide telecommunications. In those cases where an Internet service provider owns transmission facilities, and engages in data transport over those facilities in order to provide an information service, we do not currently require it to contribute to universal service mechanisms. We believe it may be appropriate to reconsider that result, as it would appear in such a case that the Internet service provider is furnishing raw transmission capacity to itself. Finally, we consider the regulatory status of various forms of "phone-to-phone IP telephony" service mentioned generally in the record. The record currently before us suggests that certain of these services lack the characteristics that would render them "information services" within the meaning of the statute, and instead bear the characteristics of "telecommunications services." We do not believe, however, that it is appropriate to make any definitive pronouncements in the absence of a more complete record focused on individual service offerings."

72 Our thinking relating to the Internet backbone points up some of the limitations of our current approaches to implementing the universal service provisions of the 1996 Act. The technology and market conditions relating to the Internet backbone are unusually fluid and fast-moving, and we are reluctant to impose any regulatory mandate that relies on the persistence of a particular market model or market structure in this area. It may be that the most successful approach in this context, maintaining universal service revenues while avoiding the imposition of inefficient or innovation-discouraging obligations, would look to the actual facilities owners, requiring them to contribute to universal service mechanisms on the revenues they receive. It is facilities owners that, in a real sense, provide the crucial telecommunications inputs underlying Internet service. If universal service contribution obligations, in the context of the Internet backbone, were based on facilities ownership rather than end-user revenues, then firms purchasing capacity from the facilities owners would still contribute indirectly, through prices that recover the facilities owners' contributions. This matter deserves further consideration.

101 We realize that, as technology evolves, new means of providing telecommunications service may emerge. Although we conclude that Internet access is not a "telecommunications service," we acknowledge that there may be telecommunications services that can be provisioned through the Internet. . . . . With respect to the provision of pure transmission capacity to Internet service providers or Internet backbone providers, we have concluded that such provision is telecommunications.

-- In re Federal-State Joint Board on Universal Service, CC Docket No. 96-45, Report to Congress (April 10, 1998)

OSP Working Paper: Digital Handshake

Partly in response to the UUNET depeerings of the late 1990s and the calls for regulatory intervention that transpired during the first Section 706 proceeding, Michael Kende of the FCC's Office of Plans and Policy (now OSP) produced an influential working paper, The Digital Handshake. He summarized his paper as follows:

In the past several years, a number of parties in the United States and abroad have questioned whether larger backbone providers are able to gain or exploit market power through the terms of interconnection that they offer to smaller existing and new backbone providers. In the future, backbones may attempt to differentiate themselves by offering certain new services only to their own customers. As a result, the concern is that the Internet may balkanize, with competing backbones not interconnecting to provide all services. This paper demonstrates how, in the absence of a dominant backbone, market forces encourage interconnection between backbones and thereby protect consumers from any anti-competitive behavior on the part of backbone providers. While it is likely that market forces, in combination with antitrust and competition policy, can guarantee that no dominant backbone emerges, if a dominant backbone provider should emerge through unforeseen circumstance, regulation may be necessary, as it has been in other network industries such as telephony.

Kende advocated for the FCC to continue with its hands-off approach to Internet services given competitive market forces.

In summary, this paper argues that if one or more backbones choose not to interconnect with other backbones for the provision of new services in the future, this is likely to be a temporary phase. This phase would end as a result of market forces that would induce backbones to interconnect, while at the same time innovative firms might step into the breach to provide interconnection services for end users. Nevertheless, during this phase there may be calls to implement some form of interconnection regulation. The paper has argued above that such intervention would be relatively unique, as there is little precedent for the regulation of networks such as the Internet where there are low entry barriers on the cost-side. In addition, regulatory intervention would be a notable shift in United States policy. As a result, any calls to intervene in the Internet market would require a correspondingly high burden of proof.

Michael Kende, The Digital Handshake: Connecting Internet Backbones, OPP Working Paper No. 32, (Sept. 2000).

- FCC Releases Study of Internet Backbone Market: Study Concludes that Competitive Internet Backbone Market Should Remain Free of Telecommunications Regulation. News Release with links to paper. 9/26/00

Section 706

Incumbent Local Telephone Companies (Incumbent Local Exchange Service or ILECs) have also tried to raise the issue of the Internet Backbone in their arguments before the FCC. The Telecommunications Act of 1996 sets for the policy goal of introducing competition into the local telephone market. The problem was how to persuade the local telephone monopoly to give up its grip on the market. The solution created by the 1996 Act was a carrot - the ILECs were be permitted to enter the lucrative long distance telephone market only when their local markets were opened up to competition. The ILECs have argued vehemently against this restraint.

This is where the Internet backbone comes in. ILECs have argued that investment in Internet backbone bandwidth is anemic and that we are on the verge of a bandwidth crisis. They have also argued that there are vast portions of this country that have no direct access to the Internet backbone (even though the entire country now has direct two-way satellite access to the Internet and, in the rural communities, the only ones complaining about this are the ILECs, not the thousands of other ISPs out there). The ILECs argue that the restraint on entering long distance service should apply to voice service only, and not long distance data, and if they were allowed to enter long distance data, they would solve the Internet backbone problem.

In the first Sec. 706 Notice of Inquiry, the FCC asked whether there was a need for the FCC to get involved in peering issues.

What can and should the Commission do to preserve efficient peering arrangements among Internet companies, especially in the face of consolidations of large proprietary gateways? We ask for comment whether the Commission should monitor or have authority over peering arrangements to assure that the public interest is served.

[First Sec. 706 NOI, para 79] The comments filed reflected rough consensus that the FCC should let the free market work; the one dissenting voice recommending FCC action was Bell Atlantic - now Verizon.

105. In the Notice, we asked whether the Commission should monitor or exercise authority over peering -- an arrangement in which two Internet backbone providers exchange traffic that originates from an end user connected to one of the providers and terminates with an end user connected to the other provider. Commenters almost unanimously oppose Commission involvement at this time in peering and similar relations among Internet firms. Only one commenter, Bell Atlantic, suggests possible action, and that is only that we "lower barriers for new entrants, in particular currently precluded entrants." We agree with SBC that premature regulation "might impose structural impediments to the natural evolution and growth process which has made the Internet so successful." Accordingly, we will continue to refrain from action involving peering. We bear in mind that "[t]he Internet and other interactive computer services have flourished, to the benefit of all Americans, with a minimum of government regulation" and that it is the policy of the United States "to preserve the vibrant and competitive free market that presently exists for the Internet and other interactive computer services, unfettered by Federal or State regulation; . . . ."

[First Sec. 706 Report, Para. 105] The FCC found that investment in Internet backbone was vigorous. More facilities are being built and those facilities have greater capacity every day. Furthermore, the FCC found that bits-is-bits. Whether its voice or whether its data, its all bits and the ILECs don't get the carrot, access to the long distance market, until they fulfill the obligations of Section 271 and open their markets to competition.

The FCC released its second 706 Notice of Inquiry in April 2000. Even though the FCC did not place the issue of Internet backbone bandwidth on the table, the ILECs nevertheless came back with arguments about an impending bandwidth shortage in the backbone. In the summer of 2001 it has been widely discussed that there is glut of bandwidth in the backbone market with tremendous amounts of unused capacity. The FCC stated: "We conclude that there has been ample national deployment of backbone and other fiber facilities that provide backbone functionality. There is no indication that specific types of areas have inadequate access to backbone or functionally equivalent facilities."See ¶¶ 20-22, 208-09

Subsequent Sec. 706 Reports (Third and Fourth Reports) have made only brief mentions of Internet backbones.

NRIC Disclosure

See also Network Disclosure

See also Industry :: Backbones (noting those networks that were found to post their peering policies)

The FCC's Network Reliability and Interoperability Council (NRIC) expanded the scope of its work with NRIC V to include packet based telecommunications. Study Group IV of NRIC V addresses interconnection and peering. In June of 2001, this study group recommended to NRIC that Internet backbones publish their peering policies. While this is merely a recommendation letter of the advisory group, it is noteworthy that the subject matter is considered properly within the scope of an FCC advisory council.

- Statement of NRIC V FG4 on Internet Peering. June 2001 ("NRIC V encourages other Internet providers, and especially the large "backbone" Internet providers that comprise the core of the modern Internet, to consider, consistent with their business practices, publication of their criteria for peering.") Availabe on the Web Archive.

- Letter from FG4 to Jim Crowe, Chair of NRIC June 21, 2001.

- Ross Callon, Scott Bradner, NRIC Focus Group IV, NRIC V Council Meeting, slide 8-9 (June 26, 2001). Copy at Archive.org

- Service Provider Interconnection for Internet Protocol Best Effort Service Network Reliability and Interoperability Council V Focus Group 4: Interoperability

- Jun 26 Network Reliability and Interoperability Council 10 am - noon. Real Audio Avail.

- NRIC Paper: Service Provider Interconnection for Internet Protocol Best Effort Service, Network Reliability and Interoperability Council V Focus Group 4: Interoperability (2001)

- FOCUS GROUP 4 FINAL REPORT APPENDIX B Proposed Outline For White Paper on Internet Peering

Service Provider Interconnection for Internet Protocol Best Effort Service Network Reliability and Interoperability Council V Focus Group 4: Interoperability (n.d.)

- NRIC Recommendations on the Posting of Peering Policies, NRIC 10/30/01

GAO

In 2001, the Government Accounting Office released Telecommunications: Characteristics and Competitiveness of the Internet Backbone Market GAO-02-16, November 14., GAO 11/14/01 in which the GAO concluded

- No publicly available data exist to allow a precise economic evaluation of the competitiveness of the Internet backbone market. However, the industry participants we interviewed generally viewed the backbone market as competitive. Several companies that purchase backbone connectivity stated that the market has become more competitive in the last few years. In particular, they noted that the price of backbone connectivity has declined, and the ability of purchasers to negotiate other favorable contract terms has improved.

- This report makes a recommendation that the FCC periodically evaluate whether existing data collection efforts are providing needed information on the Internet backbone market and, if deemed appropriate, exercise its authority to establish a more formal data collection program.

Mergers

The most significant FCC proceedings to date to address backbones have been merger proceedings (See also Industry :: Backbones listing major backbones and who has been acquired by whom). After a sufficient number of proceedings, the orders began to have stock background language that read as follows:

109. The Internet is an interconnected network of packet-switched networks. End users (individuals, enterprise customers, and content providers) typically, though not always, obtain access to the Internet through Internet service providers (ISPs) using a dial-up modem, cable modem, DSL, wireless network, or a dedicated high-speed facility (which the companies often call Dedicated Internet Access (DIA)). ISPs provide access to the Internet on a local, regional, or national basis, and most have limited network facilities. In order to provide Internet service to end users, ISPs and owners of other smaller networks interconnect with Internet backbone providers (IBPs)larger Internet backbone networks. The backbone networks operate high-capacity long-haul transmission facilities and are interconnected with each other. Typically, a representative Internet communication consists of an ISP sending data from one of its customers to the IBP that the ISP uses for backbone services. The IBP, in turn, routes the data to another backbone network, which delivers the data to the ISP serving the end user to whom the data is addressed.

110. IBPs may exchange traffic either through peering or transit arrangements. Under a peering arrangement each IBP peer will accept and deliver, without charge, traffic destined either for its own network or for one of its own backbone customers. Transit arrangements, by contrast, permit an ISP, small or regional IBP, or other corporate business, to reach the entire Internet using dedicated access lines linking it directly to the transit providers Internet backbone network. An IBP providing transit service enables the customer to send and receive traffic through the purchasers IBP to any other network or destination on the Internet. Frequently, IBP customers obtain transit packaged with a dedicated highspeed facility as part of a DIA service, with the transit customers paying fees for both the connection and the transit service.

111. IBPs generally can be categorized into tiers based on their size, geographic scope, and interconnections. Tier 1 IBPs are a small group of the largest IBPs that sell transit and/or dedicated Internet access to substantial numbers of ISPs and corporate customers or other enterprise customers. These Tier 1 IBPs peer with all other Tier 1 IBPs on a settlement-free basis. Lower tier IBPs may peer with each other, but generally must purchase transit from a higher tier IBP to reach end users that are not customers of the networks of their peers.

[SBC / AT&T Merger Order 2005] [Verizon / MCI Merger para. 110-15 2005]

The FCC made the following conclusions in the individual merger proceedings:

Mergers Between Backbones

- MCI Worldcom merger proceeding,

- MCI agreed to voluntarily divest itself of its Internet backbone, selling it to Cable and Wireless - Worldcom retained its Internet backbone services administered through its subsidiary UUNet. The FCC concluded that the divestiture of the MCI Internet backbone, which meant that the merger would not produce any increase in WCOM's Internet market share, eliminates the potential anticompetitive harms that would have resulted from the merger on the provision of Internet backbone services. [MCI/WCOM Order paras 150-156]

- The FCC agreed with MCI and Cable and Wireless that the transfer of the MCI backbone to Cable & Wireless was not a transaction that required FCC review and approval (although it was relevant to the merger of MCI and WCOM). [MCI/WCOM Order n 381]

- In response to commenters arguments that "difficulties in obtaining settlements-free peering from IBPs constitutes a substantial barrier to entry. IBPs that are unable to secure settlements-free peering agreements must use transiting arrangements, which, commenters contend, increase the costs of providing Internet services to end users and may result in poorer quality transport than that associated with peering," the FCC agreed "that peering may be a substantial barrier to entry to those firms that intend to provide Internet services. " [MCI/WCOM Order para 150]

- MCI and Cable & Wireless agree that they are prohibited from terminating their peering agreement for five years. [MCI/WCOM Order para 151]

- MCI Worldcom Sprint merger

- In 2000, the MCI Worldcom Sprint merger application was withdrawn by WCOM when the US Dept. of Justice decided that it would seek to block that merger. The Dept. of Justice stated:

WorldCom's wholly owned subsidiary, UUNET, is by far the largest Tier 1 IBP by any relevant measure and is already approaching a dominant position in the Internet backbone market. Based upon a study conducted in February 2000, UUNET's share of all Internet traffic sent to or received from the customers of the 15 largest Internet backbones in the United States was 37%, more than twice the share of Sprint, the next-largest Tier 1 IBP, which had a 16% share. These 15 backbones represent approximately 95% of all U.S. dedicated Internet access revenues. UUNET's and Sprint's 53% combined share of Internet traffic is at least five times larger than that of the next-largest IBP. The Herfindahl-Hirschman Index ("HHI"), the standard measure of market concentration (defined and explained in Appendix A), indicates that this market is highly concentrated. The HHI in terms of traffic is approximately 1850; post-merger, the HHI will rise approximately 1150 points to approximately 3000. (Note: Throughout the Complaint, market share percentages have been rounded to the nearest whole number, but HHIs have been estimated using unrounded percentages in order to accurately reflect the concentration of the various markets.)

The proposed merger threatens to destroy the competitive environment that has created a vibrant, innovative Internet by forming an entity that is larger than all other IBPs combined, and thereby has an overwhelmingly disproportionate size advantage over any other IBP. DOJ Complaint ¶¶ 32-33. More Info.

- Bell Atlantic / GTE merger (2000) The Bell Atlantic / GTE merger was approved by the FCC on the condition that GTE spin off its Internet backbone service which is now known as Genuity. This divestiture was required in order for Bell Atlantic to remain in compliance with Sec. 271 obligations. Bell Atlantic / GTE now do business as Verizon.

- WorldCom / Intermedia Merger 2001Founded in 1987, Intermedia entered the Internet market in about 1997. In addition to acquiring network services in that year, Intermedia acquired the web hosting service Digex. In 2000, WorldCom and Intermedia announced a proposed merger. On November 17, 2000, the Department of Justice appears to have filed a complaint to block the merger alleging "By adding to WorldCom's leading position in the Internet backbone market, the proposed acquisition is likely substantially to lessen competition in violation of Section 7 of the Clayton Act, as amended, 15 U.S.C. § 18." On the same day, WorldCom and DOJ reached a settlement agreement whereby they agreed that WorldCom could keep Digex, the web hosting company, as long as it divested itself of the Intermedia assets, including the backbones services. Noting these DOJ merger conditions, the FCC approved of the merger on January 17, 2001. In January 2002, the Intermedia assets were sold to Allegiance Telecommunications (and were subsequently sold to XO).

- CenturyLink 2011: In 2011, CenturyLink (formerly CenturyTel) acquired SAVVIS and Qwest. Both of those firms were considered Tier 1 backbones. However, there was no mention on Internet backbones in the FCC decisions approving the mergers. In re Application Filed by Qwest Communications International Inc. and CenturyTel, Inc.. d/b/a CenturyLink for Consent to Transfer Control, WC Docket No. 10-110, Memorandum Opinion and Order (Mar. 18, 2011); Public Notice: Notice of Non-Streamlined Domestic Section 214 Application Granted , WC Docket 11-97 (July 12, 2011) (SAVVIS)

- Level 3 / Global Crossing 2012 (approving of merger, concluding that merger is not likely to result in tipping of Internet backbone market - and noting "there have been changes in how Internet traffic is transported"

- Level 3 / TWT 2014 (approving merger without discussion of impact on backbone services market)

Access ISPs Acquire Backbones

The 2005 Mergers: 2005 saw two major mergers of the two major telecommunications companies (AT&T and Verizon), that also involved two Tier 1 backbone networks (AT&T and MCI). These two merger proceedings proceeded relatively in parallel. Both proceedings considered the implications for the Internet backbone market. Both proceedings also involved Network Neutrality conditions. The analysis in both proceedings was almost identical (the paragraph numbering was almost the same)

Access ISPs Begin to Charge Paid Peering Access Charges

© Cybertelecom ::